專家「聯」綫:投資級別債券:在挑戰中見機遇(只提供英文版本)

|

Corporate bonds with good and very good credit ratings remain an asset class of choice for investors seeking stability in their portfolios. Valuations are currently attractive, and given the loss of confidence in the US dollar, this asset class offers a good diversification opportunity in the eurozone.

Corporate bonds: better than government bonds?

Perhaps the most important feature of investment-grade corporate bonds is their low default rates. Defaults are rare and usually driven by fraud, as was recently the case with Wirecard. In addition, active security selection makes it possible to identify and avoid problem cases at an early stage. Even in the high-yield segment, driven by the overall stable economic development in Europe, there has been the exceptional situation that there has not been a single default in the eurozone in the past twelve months – even down to the CCC rating level.

As a result, some market participants already consider investment-grade bonds to be better than government bonds. It is indeed striking that some corporate bonds with globally diversified business models are offering lower yields than government issuers. For example, five-year bonds issued by French luxury goods group LVMH are yielding less than French government bonds . This is understandable from a fundamental perspective, as the business models of globally active companies are in some cases more broadly diversified than the value creation structure of a single country. In addition, the supply of new corporate bonds is lower than that of governments, especially those that want to significantly increase their debt in order to invest in defence and infrastructure modernisation. The crisis in the eurozone periphery in particular has shown that some companies can develop more stably in such a phase. In the longer term, however, it should be noted that if companies have a large part of their business model in the affected countries, it will be difficult to completely escape the negative developments on the government side. One example would be special taxes levied by the respective government to close its financing gap.

|

Euro 20 billion

In the eurozone, portfolio trades in investment-grade corporate bonds already reached an estimated volume of €20 billion in April. This means that the volume has roughly doubled compared to two years ago. This leads to a higher trading frequency: two years ago, an IG bond was not traded on average almost every third trading day, whereas now there are only about five days in ten without any transactions.

|

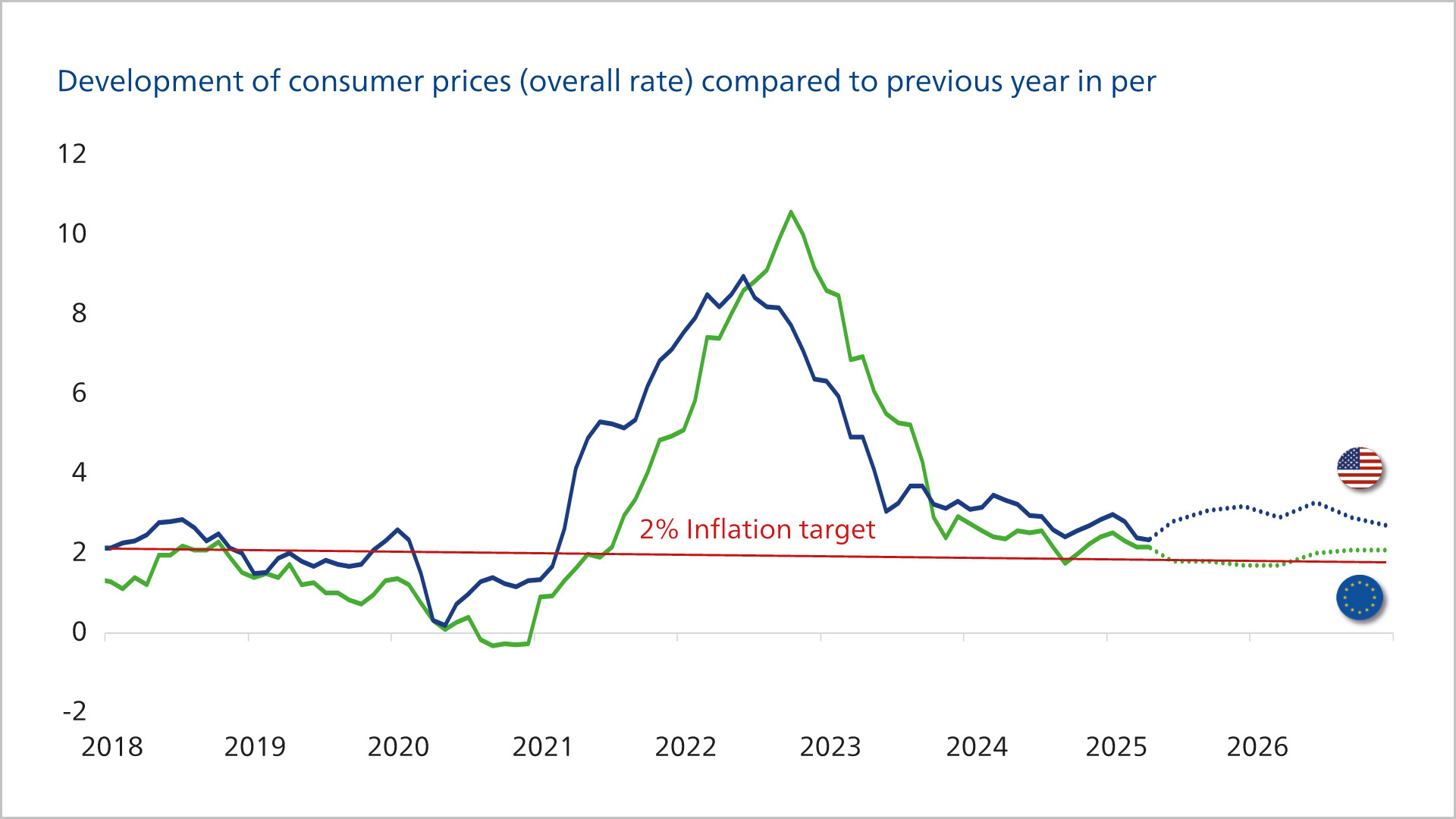

The shift away from the USD by global investors supports the medium-term outlook

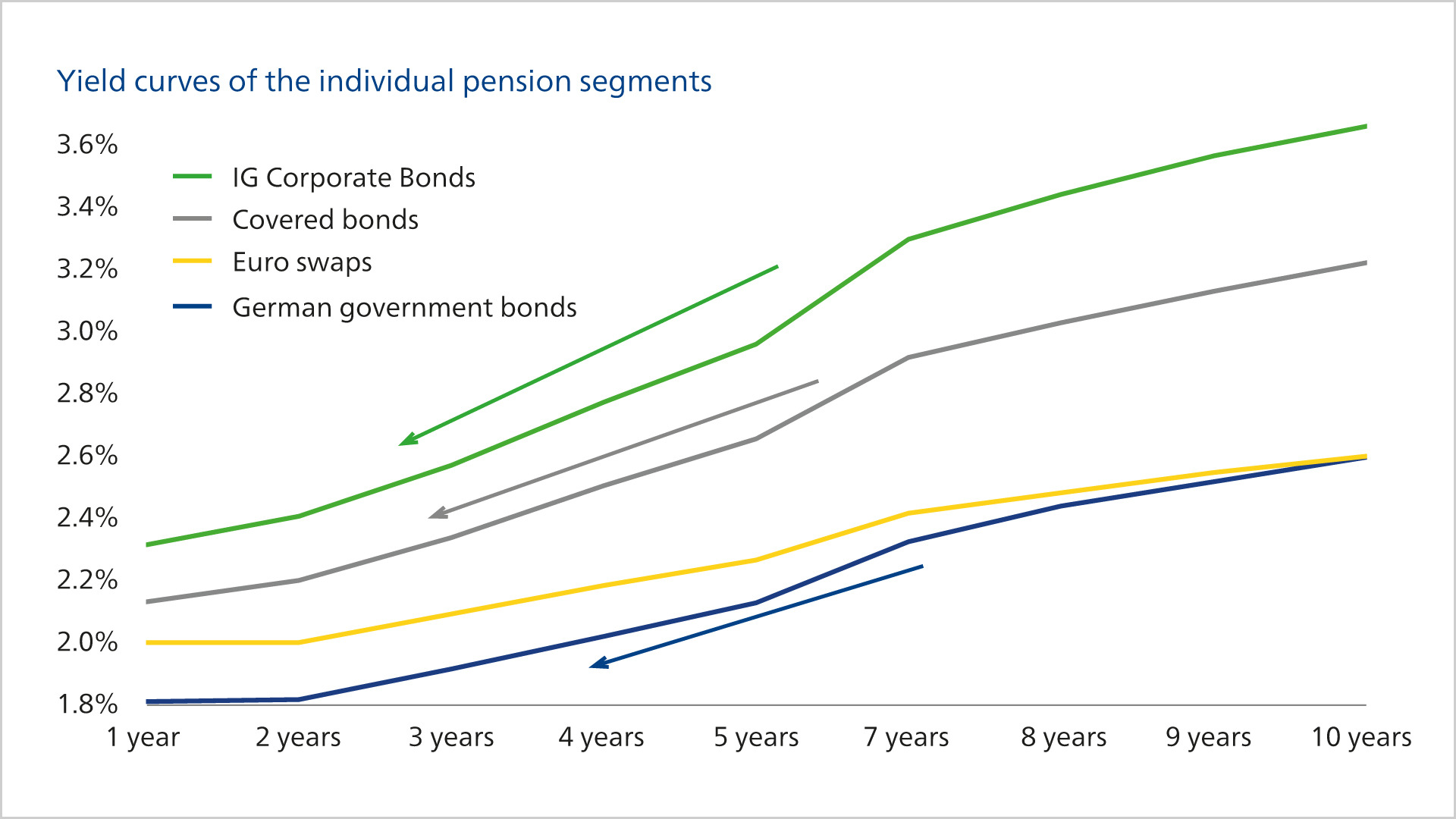

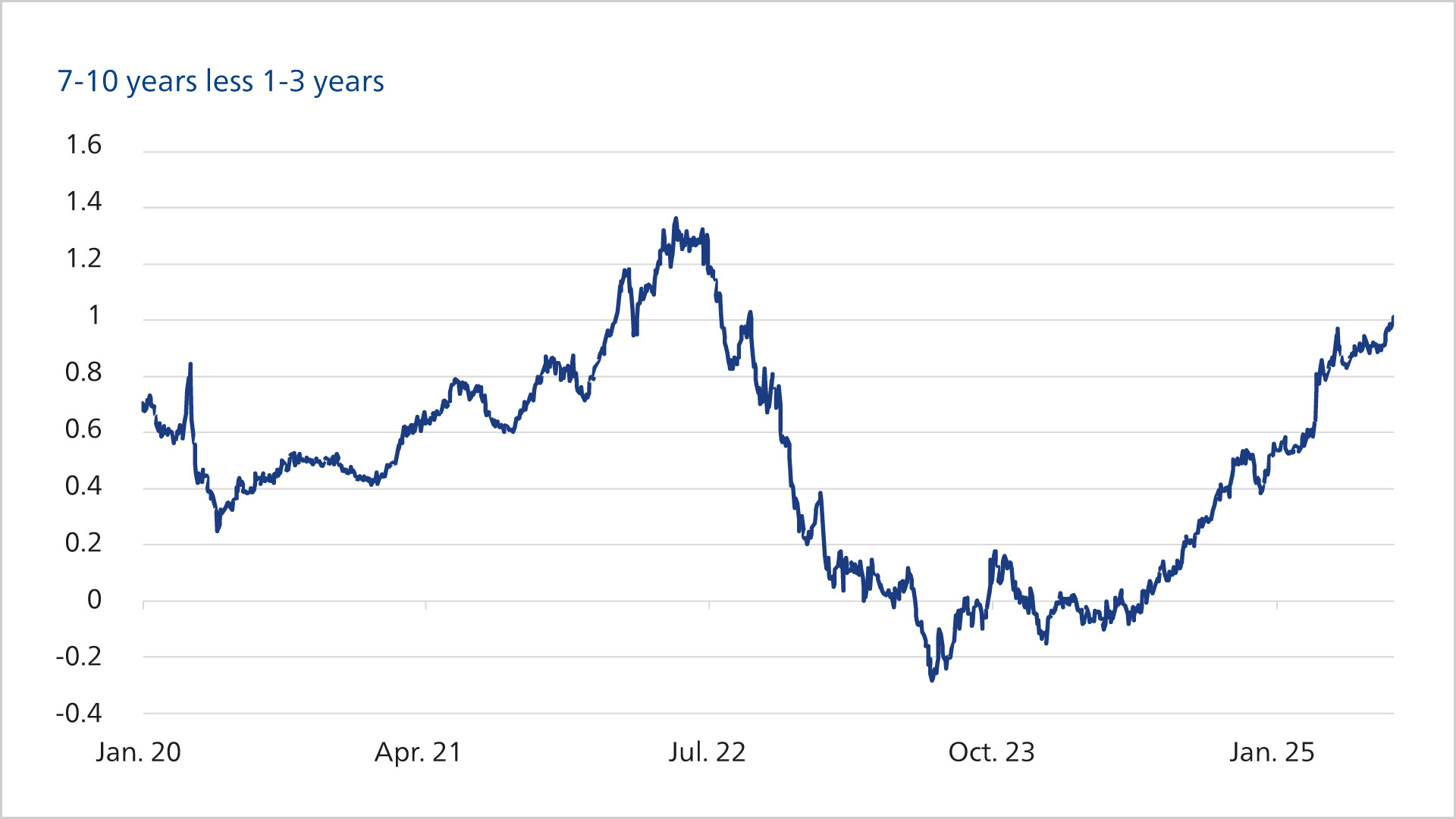

In addition, yield curves have steepened over the past two years. Around two years ago, for example, two-year German government bonds had a yield 0.8% higher than 10-year German government bonds. This effect has now reversed, and a similar trend can also be seen in the credit curves. This means that bond portfolios with largely constant interest rates over time are once again benefiting from the roll-down effect. Under current conditions, this accounts for around 0.5% of a standard corporate bond portfolio over a one-year horizon. The expected total return ( ) therefore rises from around 3% to around 3.5% over a 12-month horizon, provided that interest rates and credit spreads remain unchanged.

|

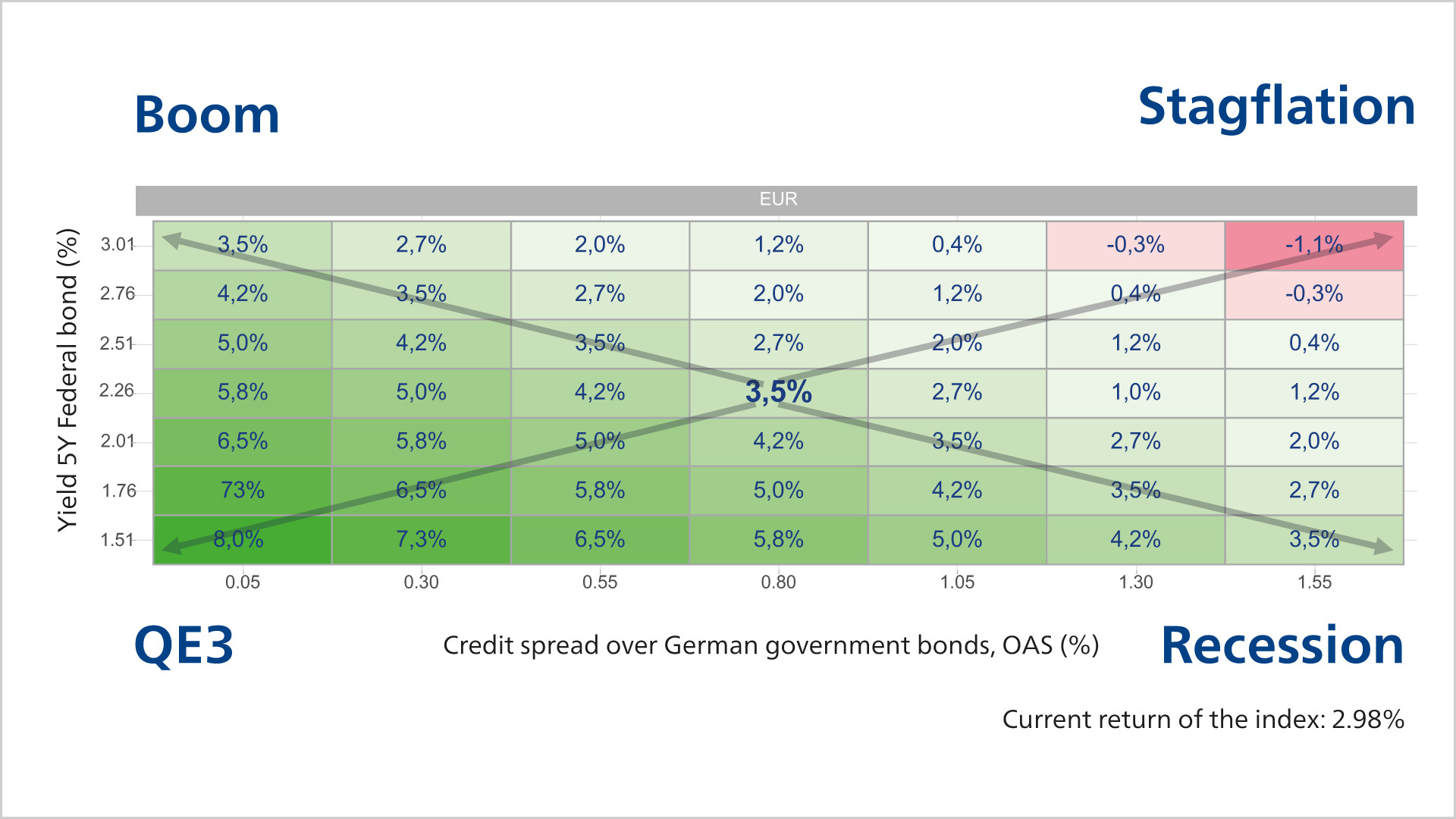

The table above calculates the 12-month return expectation for an investment in the ICE BofA Euro Corporate Index (ER00) investment-grade corporate bond index under different interest rate and spread scenarios. Current income, roll-down and the effects of interest rate and spread movements are taken into account. The X-axis represents possible credit spreads (OAS) relative to German government bonds at index level, while the Y-axis represents different interest rates for five-year German government bonds that roughly correspond to the duration of the index. Thus, if the yield remained unchanged, on five-year German government bonds (2.26%) and the credit spread over German government bonds (0.8%) the 12-month return expectation would be 3.5%. If, for example, spreads rise to 1.05% in 12 months and yields remain unchanged, the return would be.7%. 2 over a 12-month period

|

We find it noteworthy that corporate bonds offer attractive and comparatively robust earnings prospects across various economic scenarios. On the one hand, current income and roll-down effects provide a buffer against price losses, for example in the event of rising capital market interest rates.

Furthermore, correlation effects often come into play. In a boom scenario with rising capital market yields, credit risks will generally decline, thereby at least partially offsetting interest rate curve-related price losses. Conversely, in the event of a significantly weaker economic development (recession), risk premiums would rise due to concerns about a deterioration in issuers' creditworthiness. However, this effect would also be at least partially offset by the more favourable interest rate markets. A stagflation scenario is less favourable, in which interest rates remain high due to higher inflation rates, putting pressure on bond prices , while at the same time subdued economic growth is likely to lead to greater concerns about creditworthiness and thus to rising risk premiums. In contrast, a severe recession scenario, as seen during the coronavirus pandemic, is not necessarily negative from an investor perspective. In such a scenario, the European Central Bank (ECB) could not only lower key interest rates to support the economy, but also potentially enter a new cycle of quantitative easing (QE3). This would provide considerable support for bond market prices. If corporate bonds are purchased, spreads are likely to remain narrow despite the difficult economic situation, as the fundamental soundness of companies is high.

However, in line with our economists' expectations, we anticipate a moderate scenario in which the eurozone economy gains some momentum and the US economy is slowed by the trade dispute but does not slip into recession. On balance, this should lead to a sideways trend in prices and thus in yields.

Corporate bonds as a key component in a portfolio contextCorporate bonds as a key component in a portfolio context

Source: Union Investment. All information, explanations and illustrations are as at 14 July 2025, unless otherwise stated