專家「聯」綫:美元 - 避險貨幣光環褪色?(只提供英文版本)

|

Trump's frontal attack on US institutions is causing uncertainty. Confidence in the US as a "safe haven" has been damaged. The dollar is losing value. But in addition to short-term factors, there are also structural reasons for the declining dominance of the dollar. How can investors respond?

Is Trump sending the US dollar "to hell"?

"We would not really invest in a currency that is going to 'hell'." With these drastic words, Warren Buffet expressed his concern about the US dollar at Berkshire Hathaway's 60th shareholders' meeting in early May. Buffet is known to be a legend – and so has the dollar been until now. Unlike the legendary investor, however, the myth of the American currency is currently being increasingly called into question. And like so much else in recent months, this is primarily associated with Donald Trump in the public eye. Since his election in November 2024, the dollar has lost around 7.1 per cent of its value against the euro (as of 9 July) and around 12.3 per cent since Trump took office on 20 January. At first glance, it may seem obvious to attribute this development to the US government's perceived erratic economic policy. But isn't this an overly simplistic explanation? Isn't Trump merely a catalyst for a deeper, structural trend that will inevitably weaken the dollar's unchallenged position as the global reserve currency in the long run? This theory, often referred to as "de-dollarisation", has many supporters among financial market players. In this research paper, we attempt to piece together the puzzle. How can the developments of recent months be explained? And what is our long-term outlook?

We focus on two aspects: First, we examine the general role of the dollar as the global reserve currency, or in other words, the structural dominance of the dollar. One aspect of this dominance is the role of the dollar as the currency in which financial assets of the world's largest capital market, primarily US equities and bonds, are traded. We will examine this in more detail in the second part of this article, touching on the topic of US exceptionalism, i.e. the unique economic position of the United States.

When the dollar began to slide in the spring against the backdrop of Donald Trump's policies, discussions about the end of dollar dominance began in the public sphere and also in capital market circles. Occasionally, there are structural breaks that have a very rapid effect, at least on the financial market, and may explain short-term price developments. In this case, however, it is more likely to be a slow, steady adjustment process rather than an abrupt break. Nevertheless, there are a number of factors that suggest at least a moderate decline in the dominance of the dollar in the future. One of the main reasons for this thesis is the slowdown in globalisation in the wake of competition between major powers. After all, it was the more or less unrestricted globalisation of trade and financial markets over a long period of time that made the dollar almost indispensable in the first place. This is due, among other things, to the typical network effects associated with the use of the dollar in various dimensions: the more participants there are, the greater the advantages.

The emergence of political and economic spheres around the US on the one hand and China on the other will therefore reduce the network advantages of the dollar in the coming years. China and its allied countries will do everything in their power to reduce their dependence on the US in general and thus also on the dollar, meaning that there will be less globalisation and therefore fewer "participants", and the network advantages will diminish. However, given the "unfriendly" behaviour of the Trump administration in recent months, it can also be assumed that even long-standing allies of the US, such as Europe, will develop an awareness of the problem and strive for greater self-sufficiency. The point is that the dominance of the dollar – which is also established through settlement systems such as SWIFT – is so great that this replacement process will take a long time and therefore proceed very slowly. The same applies to certain underlying factors that play a decisive role in the importance of the US currency. These include, for example, the size and liquidity of the US capital market, particularly with regard to government bonds. At least in the short to medium term, there is more or less no alternative to Treasuries for the financial markets. Here, too, we therefore expect a very slow, steady process of declining dominance. In this respect, there is no really plausible explanation for a sudden decline in the dollar exchange rate.

Since Donald Trump was re-elected as US president, there have been and continue to be certain doubts as to whether this exceptionalism will continue, at least at the previous level. At the end of last year, this led to a shift from US to European equities, among other things. Suddenly, local companies were often performing better than their US counterparts. Trump's inauguration fuelled scepticism, with the new administration's trade policy in particular leading to a significant downward revision of growth forecasts for the US economy. Two other things happened at the same time: firstly, after years of stagnation, there were signs of an economic turnaround in Europe, triggered in part by the willingness of the new German government to finance large-scale infrastructure and defence investments through additional borrowing. Second, the US AI hype was dealt a serious blow by the launch of the Chinese AI model "DeepSeek," which made it clear that US AI companies had serious competition. All in all, these developments cast doubt on a supposed certainty: that it is now virtually a law of nature that US equities always generate better returns than assets from other parts of the world.

This initially had little to do with a crisis of confidence in the dollar; at the beginning of February, the dollar was still only slightly below parity with the euro. In March, however, the currency tide turned and the dollar began to depreciate against the euro. From that point until a peak in mid-April, i.e. the phase after "Liberation Day", there were two parallel developments that reinforced each other from the perspective of a euro investor: doubts about US exceptionalism in terms of stock returns and, at the same time, doubts about the special status of the dollar. This parallelism was remarkable in that it represented an atypical pattern: the dollar had long been considered a safe haven in times of crisis, meaning that when equities fell, it tended to rise or at least remain stable. This implicit hedge is one of the reasons why US equity portfolios held by foreign investors have often not been hedged against currency fluctuations in the past.In recent weeks, however, this parallel trend has no longer been evident. US equities have begun to recover and are no longer underperforming European equities (in dollar terms), and in many cases are even outperforming them again. From a fundamental perspective, this is not surprising, as US companies' earnings expectations remain robustly positive and higher than those of European companies. The relevant tech and AI stocks havebeen also in high demand again recently, especially Meta, Microsoft and Nvidia.

So, nothing but expenses? Not quite. What has not recovered is the dollar exchange rate – on the contrary, there has recently been another push towards a stronger euro. The exchange rate is now around 1.17 dollars to the euro. It can be assumed (although there is no reliable data on this yet) that this is partly due to increased hedging of the dollar currency risk. However, given the new all-time highs of US indices, it seems rather unlikely that foreign investors will continue to hold back on investments in US equities. But some investors are now no longer investing without hedging!

-

The dollar will lose some of its global dominance in the medium to long term. There are various reasons for this, some of which are independent of current political developments in the US. In particular, the greater fragmentation of the global economy in the wake of the "new" great power competition will contribute to this, because the (future) US sphere will naturally only account for part of the global trade and financial market pie. However, investors should differentiate between long-term structural developments and short-term volatility. The erosion of the dollar's dominance that is expected in the future is not in itself an explanation for the sharp short-term fluctuations we have seen over the past eight months. The former is a secular trend that will take a long time to play out. The volatility around the trend line has other causes. In our view, it shows that confidence in the dollar as a safe haven in times of crisis has been dented. In the past, US institutions have always been a guarantor of stability. However, the turmoil in April showed that, when in doubt, the US government under Trump is no longer always an anchor of stability but, on the contrary, can even be the cause of market turbulence. Trump's frontal attack on institutions increases the risk that such moments will occur more frequently in the future. In such episodes, the dollar will no longer function as a natural hedge.

-

Euro investors should therefore carefully distinguish between currency effects and the returns of an asset class in their home currency. As far as equities are concerned, doubts about US exceptionalism may have been somewhat exaggerated. There are good arguments that returns will be somewhat lower in future and that there will be a certain convergence between US and European equities . At the same time, however, the unique mix of competitive factors that companies in the US enjoy, particularly their technological lead in many areas, continue to enable to enjoythem a structural return advantage for some time to come. However, it should be increasingly questioned whether an open currency position in US equity investments continues to be a hedge against severe market turbulence. Currency hedging will therefore play a greater role for euro investors in the future.

-

Currency hedging does not come for free. The alternative is to reduce the proportion of US assets in the portfolio somewhat. On the bond side in particular, where institutional euro investors often have to hedge currency risks, this is in itself an argument for focusing even more strongly on European bonds. The already high attractiveness of euro corporates is thus further enhanced by this development.

Source: Union Investment, all information, explanations and illustrations are as of 9 July 2025, unless otherwise stated

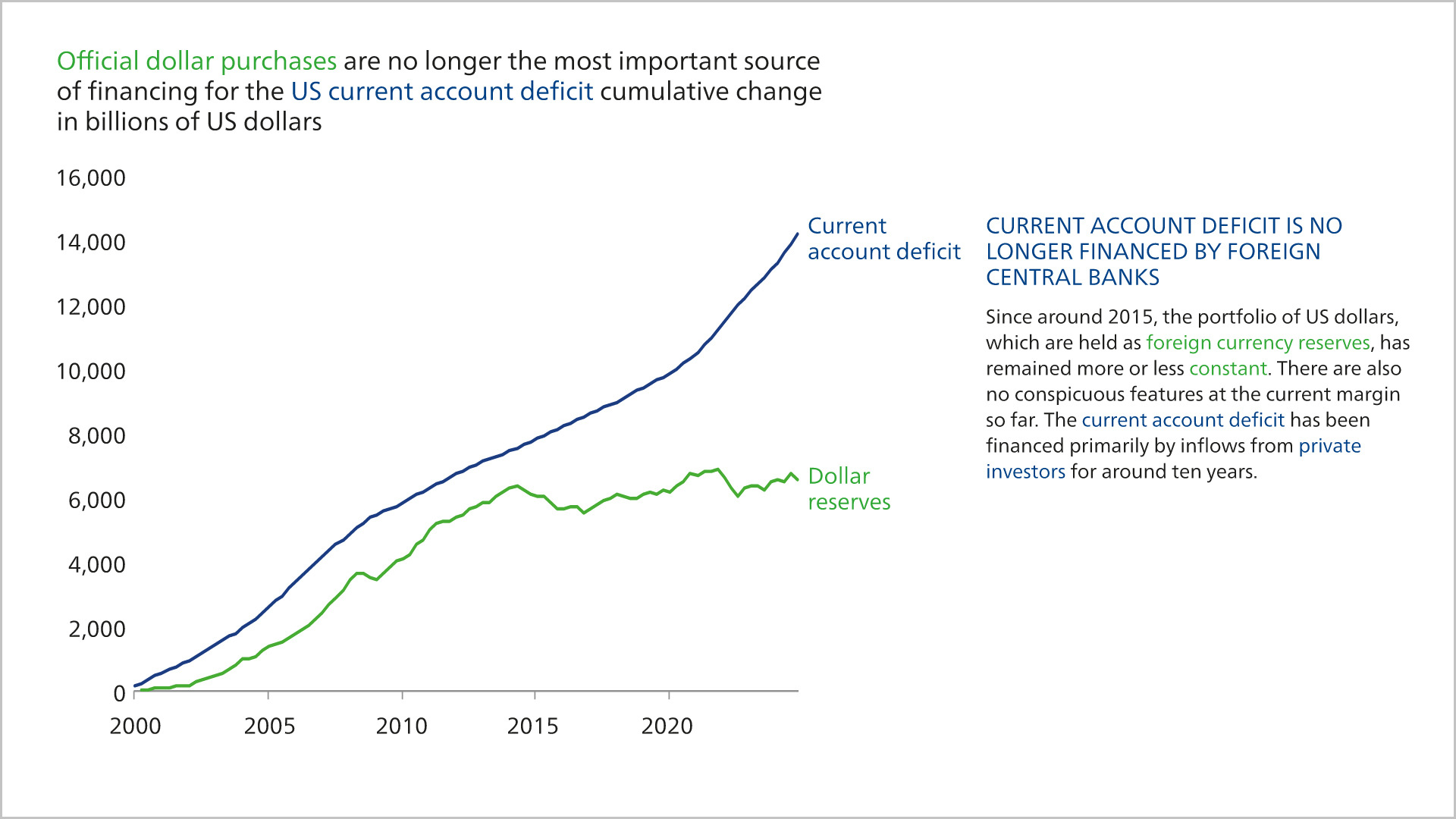

[1] Foreign currency reserves held in dollars have remained largely stable in absolute terms since around 2015. A slight decline is expected in 2025, but this is not significant in the context of the long-term trend.

[2] In literature, US exceptionalism is sometimes defined more broadly to also include the dollar and US Treasuries. Ultimately, this is a question of definition, but what is important in any case is that the reasons for the exceptional position of the dollar and US government bonds are predominantly different or only indirectly similar to those for equities.