專家「聯」綫:把握歐洲新增長動力(只提供英文版本)

|

Europe must take its future into its own hands. The security policy and economic separation of the old continent forced by the US harbors potential for new growth momentum. Investors can also benefit from this.

The erratic trade and security policy of the US is creating a great deal of uncertainty and forcing Europe to rethink its position.

On the one hand, the new US economic policy, especially the extent of the import tariffs imposed, is having a negative impact on global trade. This is affecting growth and inflation in individual countries around the world – in the US itself, but also in the eurozone.

The "great transformation" in Europe

On the other hand, the US government's shift away from Europe in terms of security policy requires economic and security reforms, such as the special fund approved in Germany to strengthen defense and infrastructure. In this context, our economists speak of a "great transformation," i.e., a new phase that could bring about a fundamental change in the economic dynamics of the old continent.

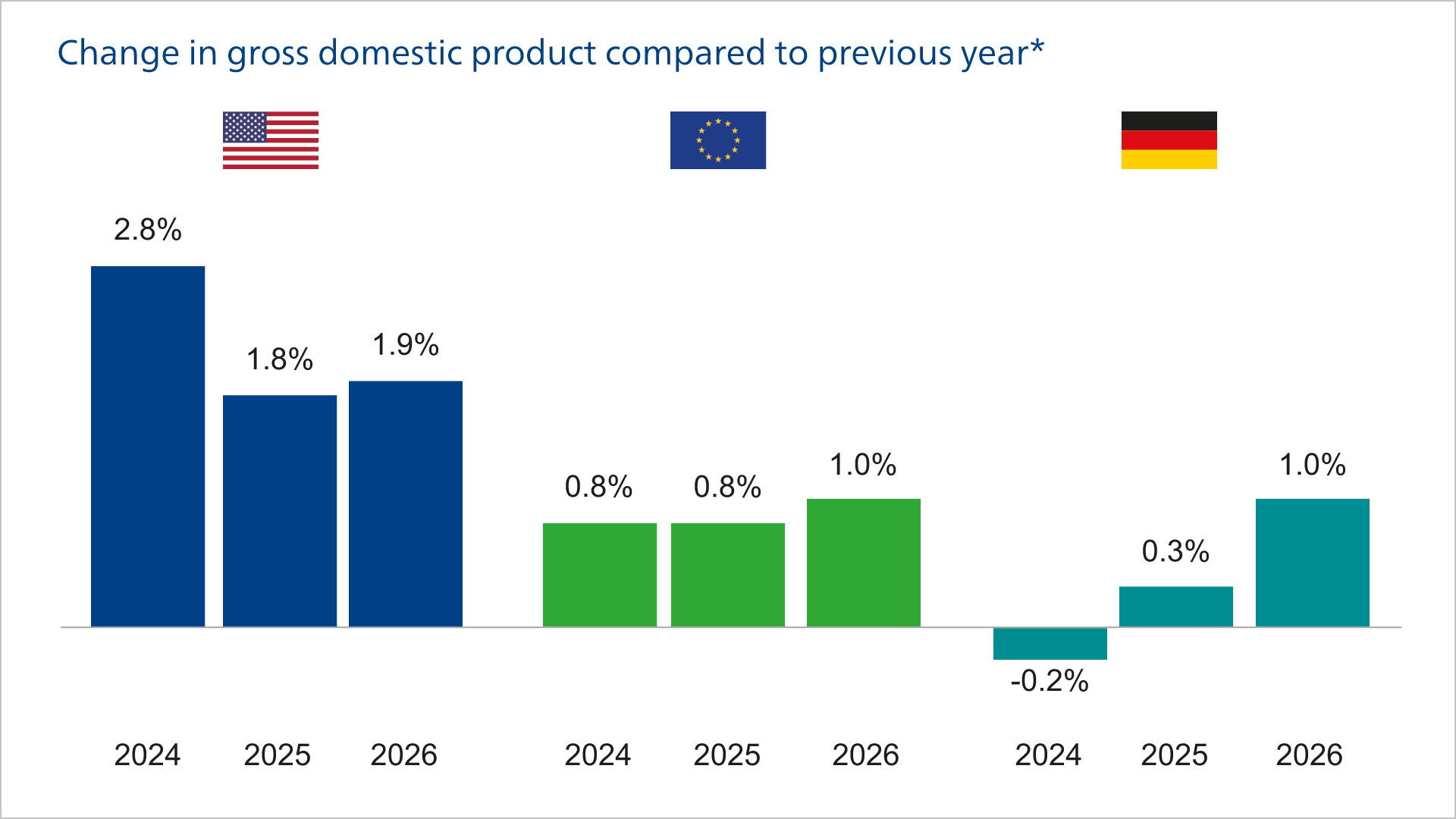

However, the looming significant increase in European defense and infrastructure spending will not have any noticeable impact on the economic outlook for 2025. In the medium term, however, there is a real chance that Europe's growth potential could rise to around 1.5 percent in the coming years thanks to improved domestic innovation in the defense sector and the associated increase in productivity.

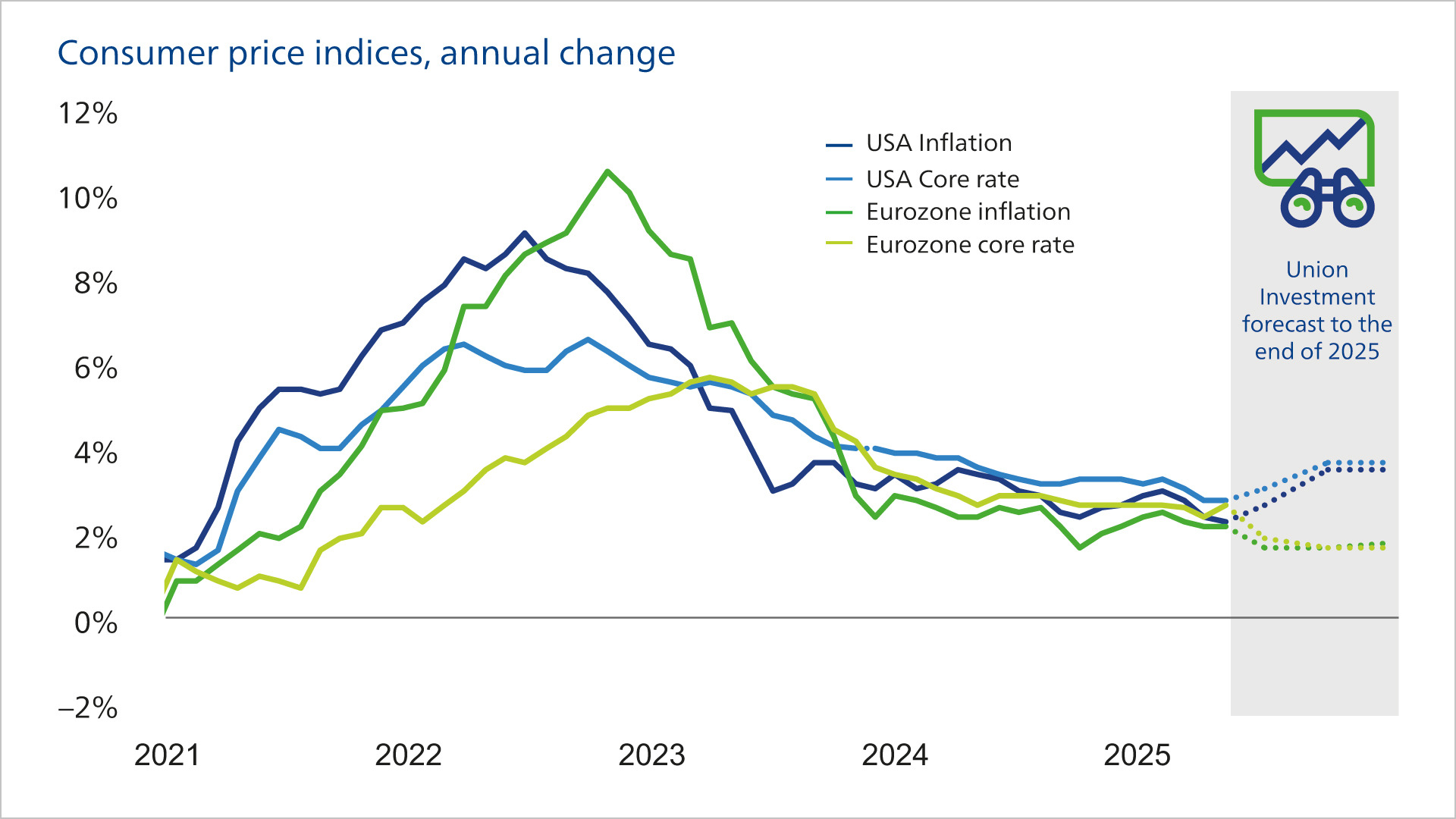

At the same time, inflationary pressure in the eurozone is likely to remain subdued. The fact that the EU has not yet imposed harsh counter-tariffs is supporting European supply chains. The economy is not currently operating at full capacity, so if there is more investment, it can be absorbed without the risk of increasing price pressure. In addition, Chinese goods are expected to increasingly flood the European market, thereby depressing price levels. The strong euro—a result of a certain loss of confidence in the US dollar—and lower energy prices are also counteracting higher inflation.

In the US, on the other hand, tariff policy is fueling rising inflation expectations, even though the tariffs will ultimately be significantly lower than initially announced following negotiations. The inflation rate is likely to remain well below the US Federal Reserve's 2% target in the coming year.

Economic growth in the US, on the other hand, is likely to slow down, as the increase in tariffs is likely to result in a significant loss of purchasing power for US consumers. However, given the fairly robust starting position of the US economy, our economists believe that a recession is unlikely.

In the eurozone, on the other hand, our experts believe that the lower price pressure and weak growth will enable the European Central Bank (ECB) to further lower its key interest rate to a landing level of 1.75 percent in June and September.

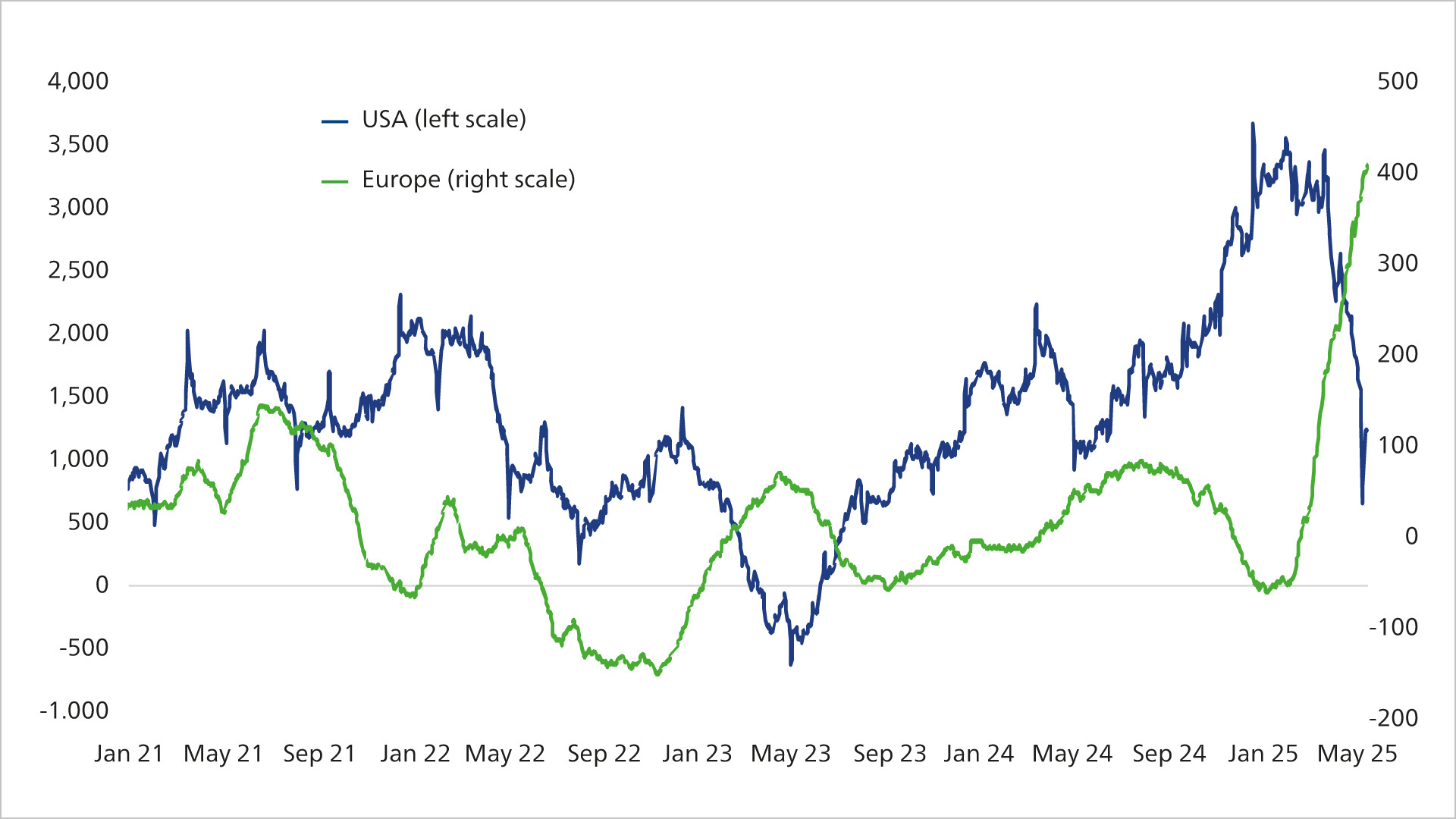

The loss of confidence in US politics observed after the US election, which intensified after “Liberation Day,” is reflected in an initial slight shift in the investment preferences of international investors: a broader diversification of assets is emerging.

This trend currently appears to be stronger than the current interest rate differential between the US and the eurozone, which, given the interest rate differential in favor of the US, would actually argue for a stronger dollar. In addition, according to standard valuation criteria, the greenback appears to be significantly overvalued compared to the euro in historical terms. This also argues in favor of a stronger euro against the US dollar in the medium term.

|

17 trillions of US dollars At the beginning of 2025, foreign investors held around 18 percent of US stocks, a record share. According to the US Federal Reserve, this corresponds to around US$17 trillion – and offers considerable potential for restructuring. |

European government bonds can be added to a global bond portfolio as a diversification option. However, given rising fiscal deficits, we continue to favor European corporate bonds with good to very good credit ratings (investment grade) and medium maturities due to their risk/return profile.

The earnings situation of companies must be assessed on a case-by-case basis. In the US, more than three-quarters of companies in the S&P 500 index and well over half of companies in the Stoxx Europe 600 index exceeded analysts' earnings expectations for the first quarter. However, companies' outlooks varied greatly and were vague. Some companies were cautious overall, while others communicated various scenarios—the possible consequences of US tariff policy are too unpredictable. From an investor's perspective, this effect makes it difficult to form expectations and thus dampens the outlook for the stock market.

Looking at individual investment styles, the expected developments point to a return of growth stocks, with growth and value stocks likely to converge in the longer term.

We expect earnings in the S&P 500 Index to rise by around ten percent in the current year, while the consensus forecast is for earnings growth of just under 7.5 percent. However, the longer the current uncertainty persists, the more earnings growth in the US is likely to lag behind overall growth. Price competition between US companies due to the varying levels of tariffs is likely to weigh on profit margins. In addition, companies with strong market positions are likely to pass on some of the additional costs resulting from the tariffs to their suppliers.

On the other side stands Europe. In the current year, profits in the EuroSTOXX 50 index on the old continent are likely to rise by around three percent, while the consensus is for stagnation. In addition to tariff policy, this is due in particular to the weak US dollar, which is weighing heavily on export-oriented companies in particular.

However, in the longer term, the expected “great transformation” with the prospect of higher economic growth potential is supporting European equities. This expectation has already been reflected in the price performance of European stocks for several months.

The market therefore believes that Europe will take greater control of its own future and leverage the resulting growth potential. However, an active investment style is needed to successfully identify the opportunities that arise. Structural changes take time to take effect, and there may be setbacks. Nevertheless, European investments are entering a more promising period in global comparison.

Source: Union Investment, all information, explanations and illustrations are as of 19 May 2025, unless otherwise stated.