專家「聯」綫:美國資金外流對美元的影響(只提供英文版本)

|

The US dollar has lost a lot of value since President Trump took office, which is down to the tariff dispute and some erratic US economic policies. International investors have started to cut back on their US investments. Even so, it's unlikely that there'll be a major shift away from the US capital market. Earnings forecasts still look good for the US.

The exchange rate of the US dollar has fallen surprisingly sharply since Donald Trump took office. Until mid-January, it was moving towards parity with the euro, with the exchange rate at around 1.03 US dollars. But then the tide turned. Since the beginning of March, the greenback has lost significant ground against all major currencies and is currently at around 1.14 US dollars per euro (25 April 2025), its lowest level in three years. This development is primarily the result of the tariff conflict initiated by Donald Trump. 2 April was a moment of shock for global capital markets. Even though Trump has postponed most of the tariffs for three months for the time being and promised bilateral negotiations with many trading partners, confidence in US economic policy has been shaken.

At Easter, Trump added fuel to the fire with statements that fuelled fears that he might try to dismiss US Federal Reserve Chairman Powell. Although Trump soon denied this, a bitter aftertaste remains. Under current law, it is virtually impossible to fire the head of the Federal Reserve. Powell will only remain chairman of the US Federal Reserve's Board of Governors for around another year, but is expected to remain a member of the governing body until 2028. However, the fact that Trump has even raised the issue of the Fed's independence is leaving its mark on the capital market. As a result, yields on long-term US Treasuries initially rose sharply.

Foreign countries are reducing their US investments

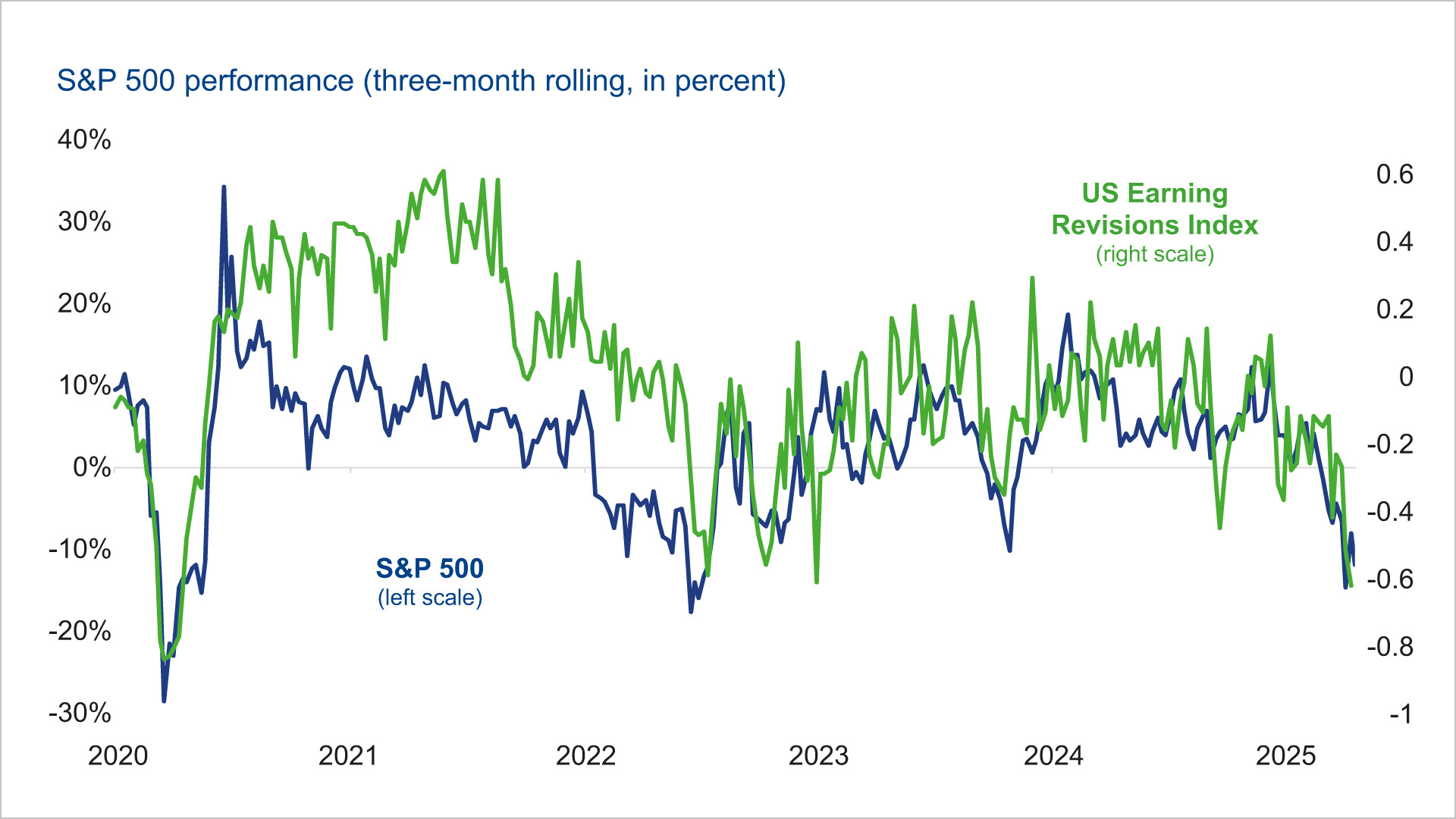

As a result of the significantly increased uncertainty caused by the constantly changing announcements on US tariff policy, international investors divested some of their investments in the US capital market. It should be noted that they had also built up very high overweightings in the US in recent years, as the US markets had long offered the highest returns. The technology and artificial intelligence rally surrounding the major US tech companies (Magnificent Seven) lasted for years and was only halted at the end of January this year by the market entry of the Chinese AI model DeepSeek. In addition, important benchmarks such as the MSCI World Index consist of around 70 per cent US equities.

Many investors have clearly drawn an important conclusion from the last few weeks: with Trump's erratic style of government and the daily changing news situation, the risks for investments in the US must also be reassessed. This applies to all asset classes, not just the exchange-traded segments.

Looking at the individual market segments, it can be seen that European investors were (and still are) particularly heavily invested in US equities, while the majority of US government bonds held abroad (around 30 per cent) are held by institutional investors in Asia, particularly Japan and China. According to our current assessment, the recent dynamic weakness of the US dollar against the euro and yen is mainly due to the reduction in US equity holdings by international (and also European) investors.

Even though there was a significant rise in yields on the US bond markets at the beginning of April, particularly for long maturities, the situation has initially calmed down thanks to the monetary policy anchoring of short maturities. Short-term action by central bank reserve managers in US dollars is unlikely and not currently visible. However, it remains to be seen whether these strategically oriented players will change their investment behaviour in the future. For example, China, the second-largest foreign creditor of the US, has been reducing its US Treasury holdings for several years, albeit in a market-friendly manner and in small steps. This is probably being done by not reinvesting maturing US government bonds.

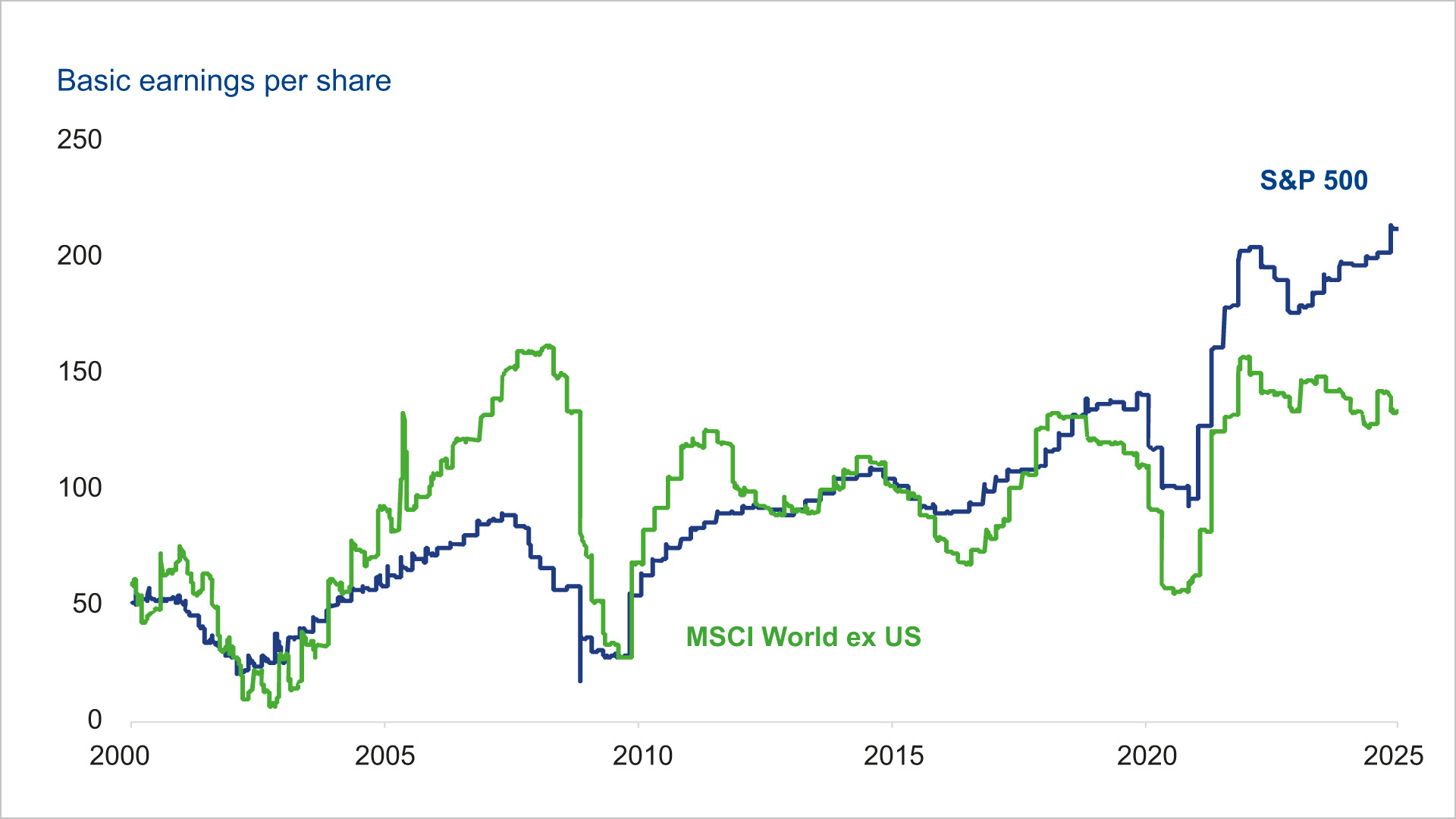

Profit growth for three years only in the USA

Source: Union Investment, all information, explanations and illustrations are as of 28 April 2025, unless otherwise stated