專家「聯」綫:歐元股票繼續上漲(只提供英文版本)

|

European stock markets, in particular the DAX, have performed positively since the beginning of the year and are regaining international investor interest. Despite ongoing economic and political challenges, European equities offer a certain catch-up potential with lower valuations than US markets.

Since the beginning of this year, the European stock markets – in particular the German leading index DAX – have performed significantly better than the US stock markets. This has interrupted a multi-year phase of underperformance. International investors have rediscovered Europe after avoiding it for years. This is surprising given the many economic and political challenges facing the 'Old Continent'. Economic growth remains subdued, bureaucracy is high and political polarisation is increasing. In addition, the major technological innovations of recent years have mostly come from the US. In this context, China is also catching up more and more. For example, low-priced Chinese e-cars are making life increasingly difficult for established European carmakers. Furthermore, demographic trends in Europe are significantly less favourable than in the US. And since the beginning of the war in Ukraine, the loss of cheap energy supplies from Russia has led to a noticeable increase in energy costs. On top of that, the new US administration is now making life difficult for Europeans. It is not yet clear how high US tariffs on European cars and other goods will ultimately be. In any case, there is currently a great deal of uncertainty surrounding Trump's trade policy.

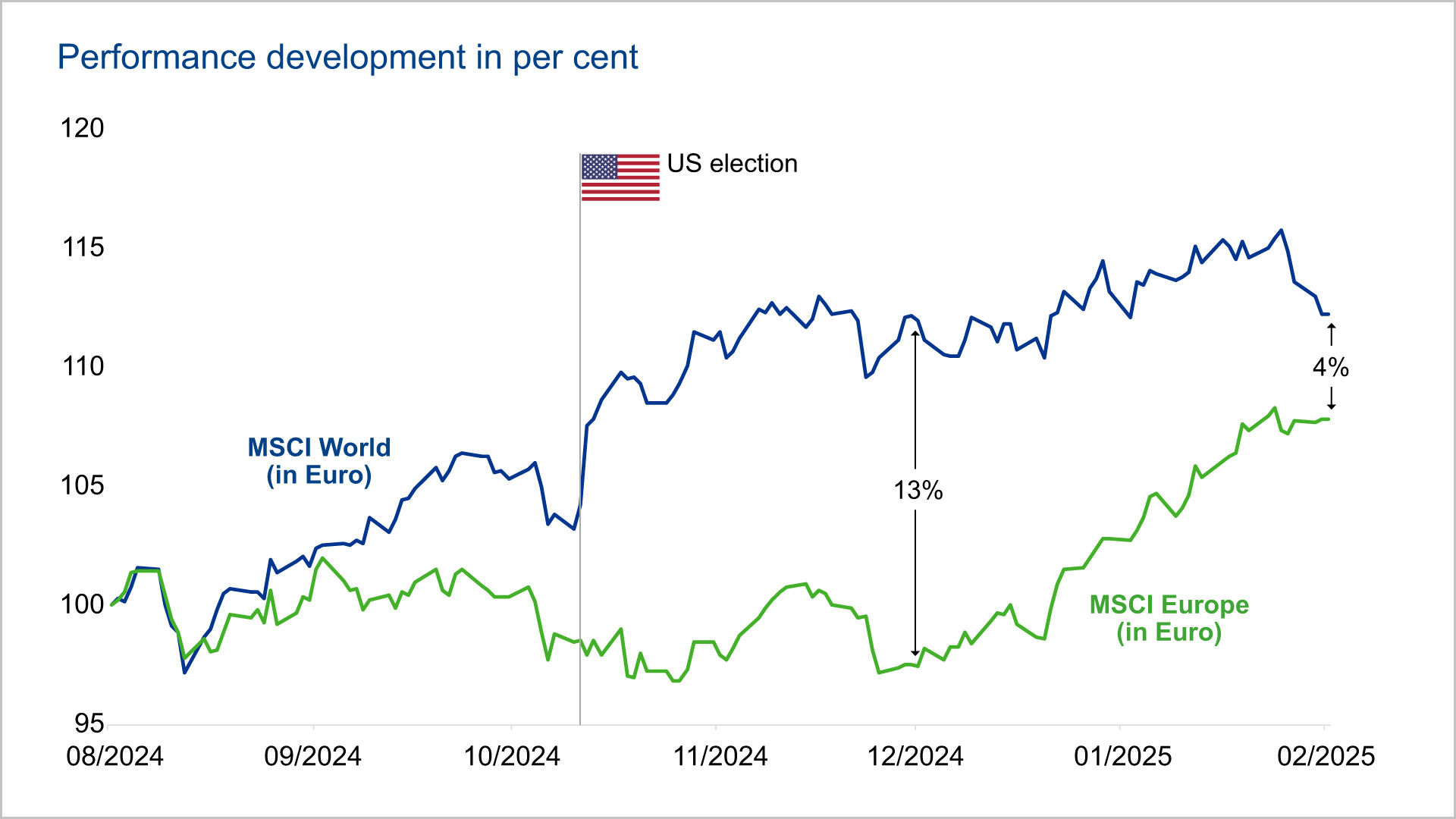

Europe's stock markets have caught up in the short term.

The gap between Europe and the MSCI World has been closing since the beginning of the year.

In Europe, by contrast, the situation has long been characterised by a great deal of uncertainty. The war in Ukraine, economic stagnation in the core countries and the weaker corporate earnings trend weighed on share prices. There have been huge outflows of funds since the beginning of the war in Ukraine. For a long time, international investors were underinvested in Europe, while the US stock markets ran ahead. This resulted in the valuation of European equities diverging further and further from that of US equities. The capital outflows from Europe were one reason why, in addition to the weaker price performance of equities, the euro exchange rate against the US dollar also weakened.

However, since the election of Donald Trump in November 2024, the markets have started to move. Gradually, more investors have returned to Europe. The chances of an early end to the war in Ukraine have increased. This would reduce the risk premium on energy commodities, as more Russian oil and gas could flow to Europe again. The decline in input costs would strengthen Europe's competitiveness.

At the latest since the Munich Security Conference, it has also become clear that Europe will have to pay more for its own defence. As a result, the political will is growing in the European Union (EU) to take on joint debt in order to finance rearmament. The result of the German parliamentary elections also points in this direction. It is already foreseeable that the new government will network more closely at the European level.

With regard to European companies, many sectors have now emerged from the valley of tears. One example is the chemical industry. High energy prices had made exports uneconomical. Companies had to adjust their capacities to local conditions. This transformation has now progressed so far that the companies are profitable again. In this environment, the possible end of the war in Ukraine could be a strong catalyst for share prices. A similar picture is emerging for carmakers, who are operating in a very challenging environment. There is now a growing chance that the EU could back away from its strict CO2 regulation. This prospect has recently boosted the sector.

European equities still have some catch-up potential

In summary, there are many factors in favour of investing in Europe and particularly in Germany: an end to weak growth, the proposed relaxation of Germany's debt brake, the possible end of the war in Ukraine and the associated decline in the risk premium on energy prices, the reconstruction of Ukraine, the necessary military build-up in Europe and the localisation of value chains (re-shoring of production facilities).

In addition, monetary policy could be a positive driver. The US Federal Reserve has recently adopted a more cautious approach and refrained from further interest rate cuts. The background to this is the stubborn US inflation, which is likely to be further fuelled by Trump's tariff and fiscal policy. In contrast to the market consensus, the economists at Union Investment therefore do not expect interest rates to be cut in the US this year. By contrast, the European Central Bank is likely to continue its policy of lowering interest rates, as both growth and inflation remain subdued in the eurozone. These interest rate cuts could have a positive impact on the more cyclical European stock markets.

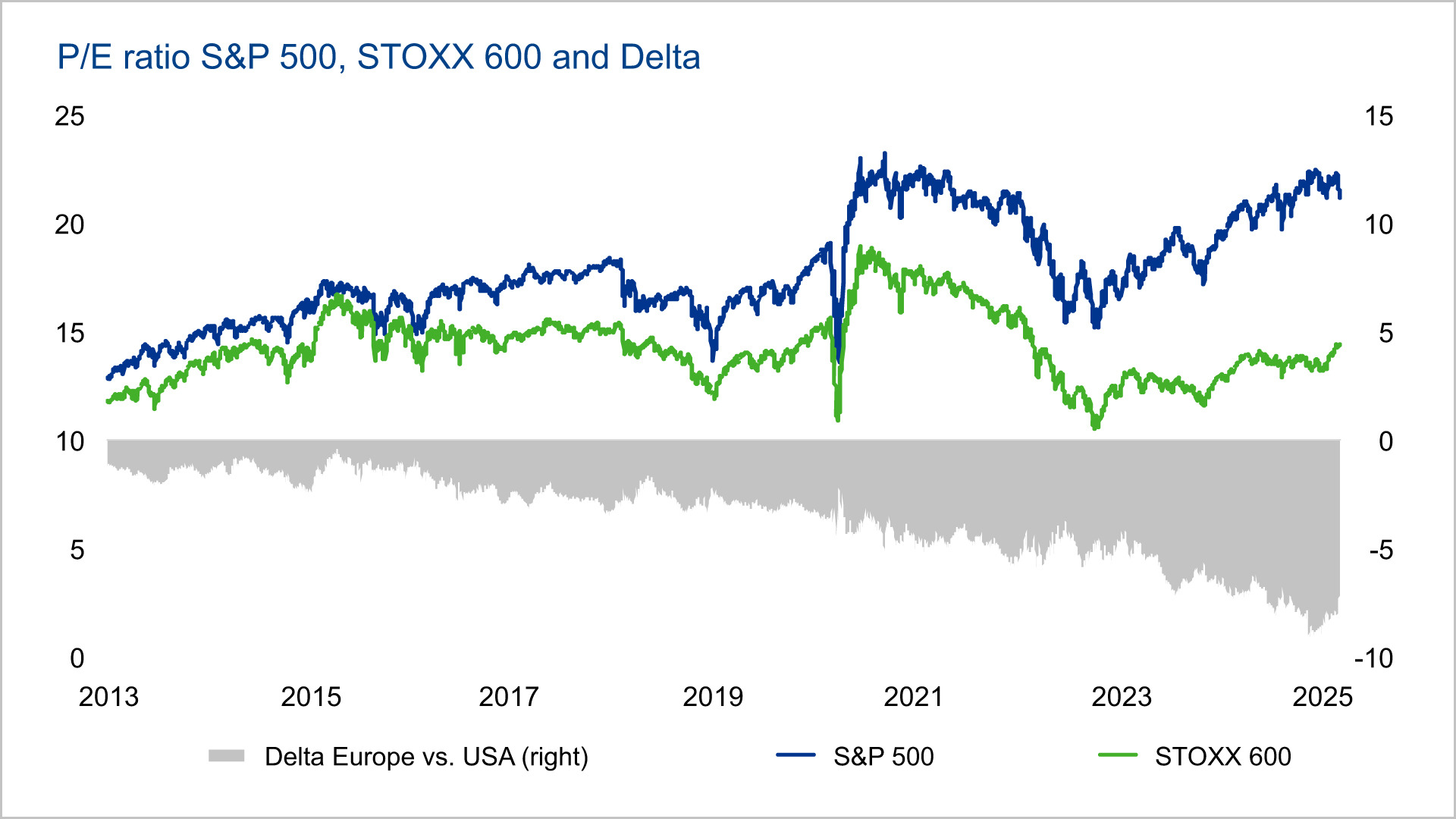

All these factors come on top of the relatively low valuation of European equity markets. The average price-earnings ratio (P/E) for the MSCI Europe index is currently 14.6 times on a 12-month horizon. The MSCI World Index is valued at 19.4 and the S&P 500 at 21.7. However, this is partly justified by the fact that earnings growth in the US this year is almost twice as high as in the eurozone, as the growth gap remains wide open.

Europe with significant valuation discount vs. USA

Conclusion: active asset management can make all the difference. According to the experts at Union Investment, there is still some room for manoeuvre on the European stock markets. The key drivers in the coming months are likely to remain, on the one hand, the US tariff issue and, on the other, possible peace negotiations in the Ukraine war. Both are subject to a great deal of uncertainty, so there is also potential for disappointment here. This is because expectations have risen since the beginning of the year. Overall, the experts are cautiously optimistic and expect slight price increases for German and European equities by the end of 2025. However, the upward trend is likely to flatten as the year progresses.

Source: Union Investment, all information, explanations and illustrations are as of 3 March 2025, unless otherwise stated