Union Connect: Navigating a stock portfolio through volatile periods

|

Volatility on global equity markets is increasing. Investors should be aware of different investment styles being crucial to investment success in the short term. Those who focus on long-term returns and prudent risk management should diversify across several dimensions.

The world has been a different place since US President Donald Trump threatened his most important trading partners with enormous trade barriers in April. Since this so-called "Liberation Day", at the latest, it has become clear to everyone that we are witnessing a reversal of globalisation. Global supply chains and production sites around the world are apparently a thing of the past because the associated risks are no longer calculable for many corporations.

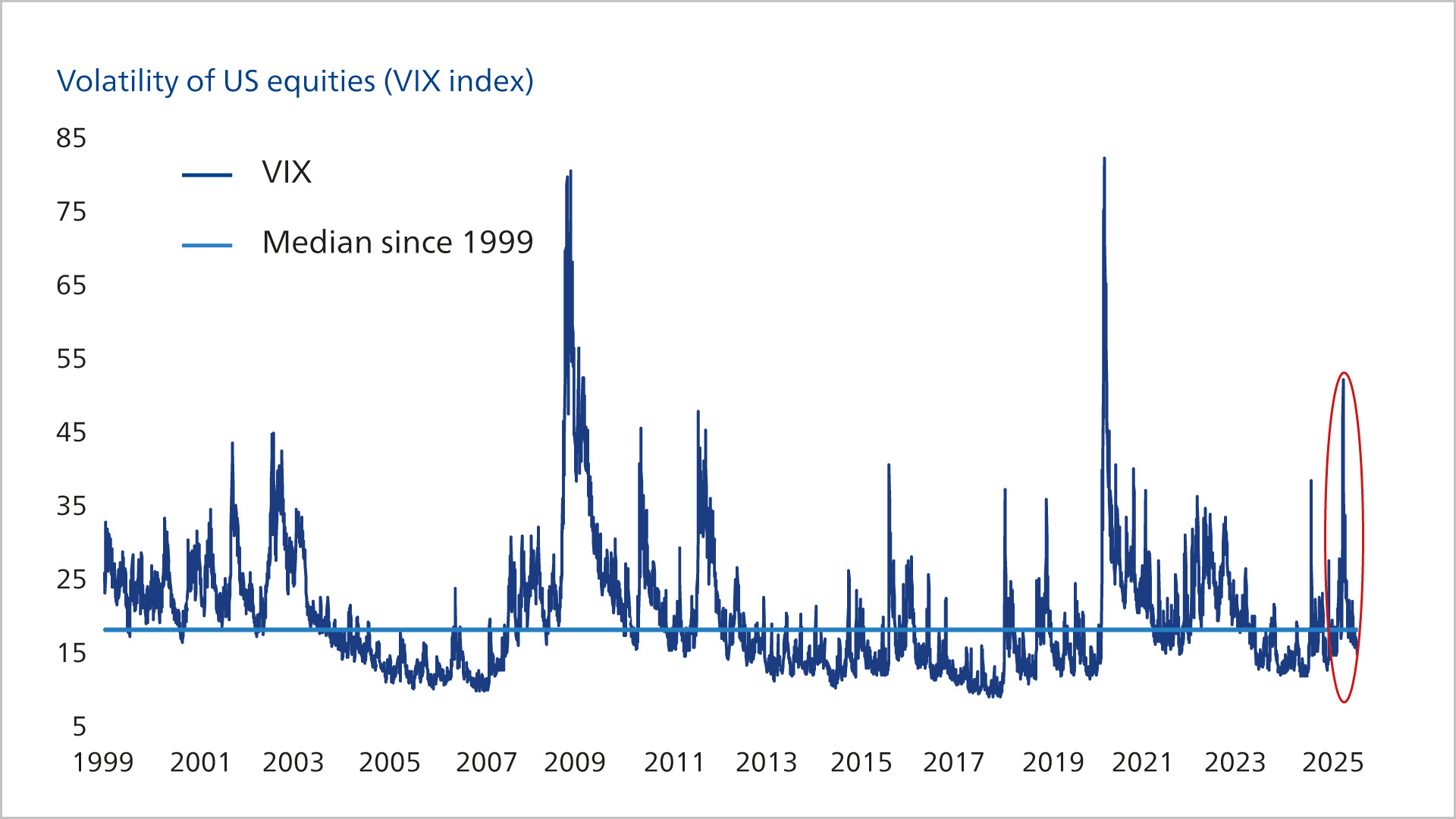

Stock volatility with sharp swings around “Liberation Day”

With the recovery on the stock markets, volatility has fallen significantly again.

Source: Bloomberg, Union Investment; as of July 31, 2025.

|

89.53

The CBOE Volatility Index, or VIX for short, reached its record high of 89.53 points on 24 October 2008. It was the height of the financial crisis, when fears of further bank collapses were rife. A few weeks earlier, the US investment bank Lehman Brothers had collapsed and nervousness in the financial sector was correspondingly high. The record high in the volatility index was only surpassed on 20 October 1987. It was the Tuesday after Black Monday on Wall Street, when the VIX rose to a dizzying 172.9 points. Unlike today, however, the index was calculated on the basis of the S&P 100 at that time. Since 2003, the broader and more meaningful S&P 500 has been the basis for calculating the world's best-known volatility index.

|

Changing macro conditions are affecting markets

Investors should prepare themselves for the fact that markets will not only be more volatile than usual on individual days. The VIX index, which tracks the volatility of the US benchmark index S&P 500, is often used as a benchmark for this. Whereas in the past a level of ten to twelve points was considered normal, we are likely to see 15 points or more as the norm in the coming years. The main reason for this is the economic conditions, which are rubbing off on the markets. Uncertainty in supply chains and the limited supply of cheap energy mean that production in the various economic regions is being scaled back in line with demand, and even small changes in the availability of raw materials or intermediate products, for example due to regional crises, can lead to prolonged production problems . All this is exacerbated by the erratic trade policy of US President Trump, which is making planning much more difficult for globally active stock corporations.

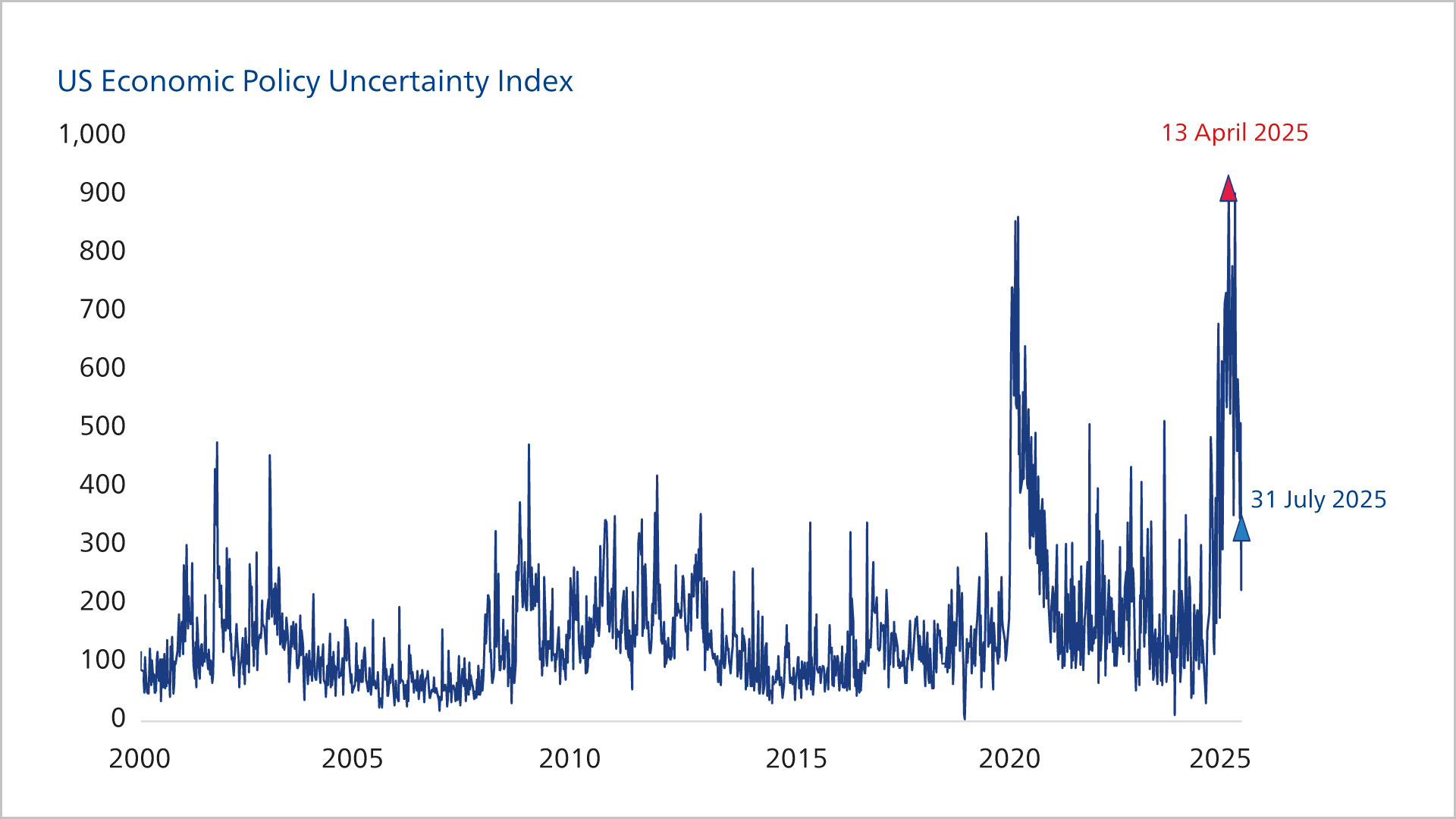

Political uncertainty much higher than in Trump's first term

Despite decline, still at elevated level

Source: Bloomberg, Union Investment. As of July 31, 2025.

Investors who put their money into stocks should therefore start thinking about strategies for dealing with increased volatility. But first, three things need to be said.

1. In recent years, increases in volatility have often turned out to be good buying opportunities. Even though it is tempting to hedge and sit on the sidelines, it is not necessarily advisable for long periods of time to remain inactive. Investors who have little tolerance for volatility can use option strategies to bring stability to their portfolios rather than removing entire positions in risky securities from their portfolios. This is because the markets tend to overreact, as seen on "Liberation Day", and price in very bad news. If things do not turn out to be as bad as expected, they price out the risks again. This can be seen, among other things, in the fact that the tariff threats since "Liberation Day" have been taken in stride in terms of the intensity of the price swings – the markets are also learning.

2. Given the structurally higher volatility, it is important to diversify the portfolio broadly in order to hedge against risk. Technology stocks are currently calling the shots and remain an important component of any portfolio. However, they can be complemented by more defensive stocks, such as those in the insurance or pharmaceutical sectors. The same applies to cyclical industries, which can benefit from rising infrastructure and defence spending. What applies to different sectors should also apply to investment regions and styles.

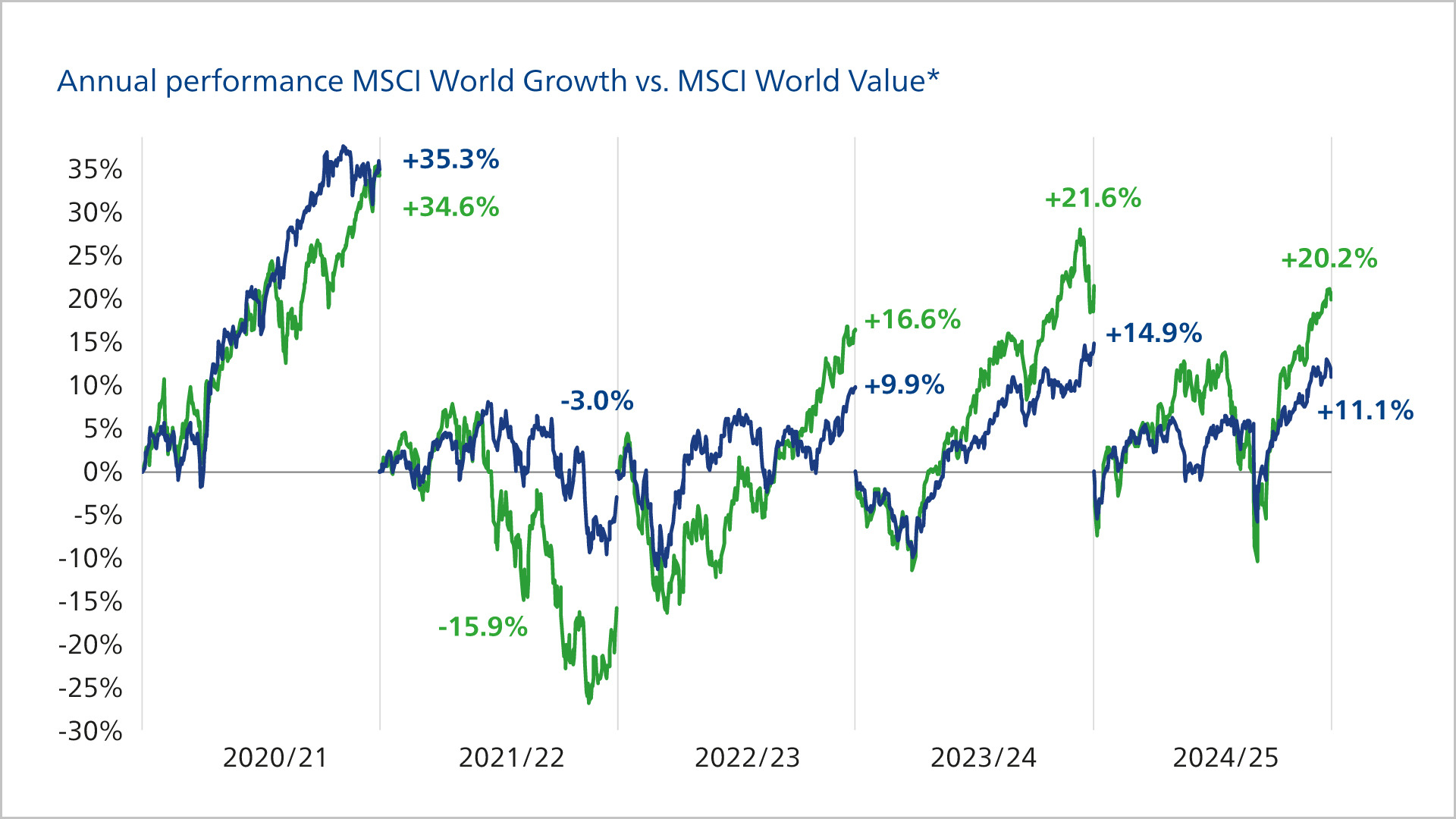

Combining several investment styles, regions and sectors may sometimes reduce returns in short market phases if one sector outperforms all others. However, this means that the risk is better spread for investors with a long-term horizon. It is important not to look at regions and sectors in isolation, but to have a mix of high-growth (growth) stocks and more attractively valued but fundamentally sound (value) stocks in the portfolio. There have been plenty of examples of one style outperforming the other in the past. Just think of the long-term outperformance of growth stocks in 2024, whose boom came to an abrupt end, at least temporarily.

Combining several investment styles, regions and sectors may sometimes reduce returns in short market phases if one sector outperforms all others. However, this means that the risk is better spread for investors with a long-term horizon. It is important not to look at regions and sectors in isolation, but to have a mix of high-growth (growth) stocks and more attractively valued but fundamentally sound (value) stocks in the portfolio. There have been plenty of examples of one style outperforming the other in the past. Just think of the long-term outperformance of growth stocks in 2024, whose boom came to an abrupt end, at least temporarily.

A blend strategy can bring stability to your portfolio

Frequent changes in favorites between growth and value stocks

Source: LSEG, Union Investment. As of July 31, 2025. * In each case in the net return variant. Period under review: July 31, 2020 to July 31, 2025, in one-year segments. Performance data is based on past performance and is not a reliable indicator of future performance.

Looking ahead, quite a few analysts see long-neglected stocks in the infrastructure segment as frontrunners in the medium term, because they stand to benefit from infrastructure and defence spending, not only in Europe but especially there.

3. When selecting individual stocks, investors should pay attention to how well companies themselves are able to hedge against more pronounced market volatility. How stable are their supply chains, and how vulnerable are they to shocks, geopolitical crises or rapid currency fluctuations? After all, you can only recognise real opportunities if you look beyond sectors and styles and focus on the companies behind them. Even with moderate volatility, the dispersion between the best and worst companies in an industry can sometimes be enormous. That is why, regardless of whether the markets are more volatile or not, careful stock selection is essential for successful investing in the stock market.

In order to interlink the changed investment world with its influences from macroeconomic structural breaks and the idiosyncratic company level, a combined approach of top-down and bottom-up analysis is recommended. For example, the macro investment strategists at Union Investment develop forecasts for economic growth and inflation and calculate probabilities for various scenarios, such as unexpected sharp changes in the interest rate environment or geopolitical crises. The strategic perspective is combined with a fundamental analysis of individual companies. They are examined in terms of their resilience to macroeconomic changes, the quality of their business model, their balance sheet structure and various valuation ratios, and then compiled into a global portfolio.

Source: Union Investment. All information, explanations and illustrations are as at 14 August 2025, unless otherwise stated