Union Connect: Fixed Income Outlook

|

The most important information for you in brief

|

The central banks' current interest rate reversal is having a significant impact on the bond market. Four theses on how it will continue and what is different this time.

For ten years, the European Central Bank (ECB) kept its deposit rate at zero per cent or in negative territory. Then came the sharpest interest rate turnaround since German reunification. Now another interest rate turnaround is in full swing. After the first interest rate cuts by the ECB and the Federal Reserve, and in anticipation of further cuts, yields have already fallen significantly. The high current interest rate and the capital gains resulting from the decline in yields have led to extraordinary investment performance: euro-denominated corporate bonds with good credit ratings yielded more than 10 per cent over the last twelve months. What is in store for the bond market?

1. Monetary policy is shifting its focus from inflation to economic growth.

This was clearly expressed in Fed Chairman Jay Powell's speech at the Federal Reserve Bank of St. Louis's annual meeting in Jackson Hole (USA) in August this year, but also in statements by ECB Chief Economist Philip Lane. This assessment is shared by the capital market, as the development of inflation expectations shows.

Inflation rates have fallen significantly.

Consumer price indices in the US and Europe, annual change

Source: Bloomberg; as of 4 October 2024.

While the fight against inflation seems to have been largely won, a certain cooling of the economy is now becoming apparent. For the US Federal Reserve, the consequence is clear: monetary policy must shift its focus from inflation to the labour market and, if necessary, cut key rates quickly if unemployment continues to rise and employment growth slows. The ECB's response is less forceful. As Executive Board member Isabel Schnabel never tires of mentioning, the economic downturn, particularly in Germany, has structural causes that cannot be influenced by an easing of monetary policy. However, the ECB will not be able to ignore the economic slowdown in the euro area either, as it is likely to contribute to falling inflation rates in the medium term.

How much and how quickly the central banks lower their key rates in the future will therefore depend increasingly not only on inflation, but also on economic developments. The fact that this is a double-edged sword was demonstrated at the beginning of October: after the surprisingly strong increase in employment in the US, the market priced out future interest rate cuts again and yields rose.

2. Bonds offer asymmetrical opportunities for price gains

Not only the US Federal Reserve and the ECB, but also the Chinese central bank and many other central banks around the world are increasingly turning their attention from inflation to the economy. This shift in focus offers opportunities for bond holders, because the current interest rate level is restrictive according to the unanimous opinion of monetary policymakers. The neutral interest rate cannot be determined unequivocally – in the US it is likely to be around three per cent, in any case not at the current level of 4.8 per cent. For the euro area, the neutral key interest rate is estimated to be around two per cent, which is also well below the ECB's current deposit rate of 3.25 per cent. The two major central banks thus have plenty of room for monetary easing and can lower their key interest rates below the neutral level if necessary.

The bond market has already anticipated future key interest rate cuts to a considerable extent. A key interest rate of 3.4 per cent in the US and less than 2.0 per cent in the eurozone is priced in for the end of 2025. It is quite possible that the central banks will lower their key rates to this level and no further. In that case, holding slightly longer-dated government bonds would no longer yield more than an investment in the money market.

So, safe bonds with longer maturities offer no guarantee of further price gains, but they do offer an option on them. Should the economy cool noticeably, most central banks have room to lower their key interest rates much more quickly than is currently priced in. In the likely scenario of calm economic development, bonds will therefore yield adequate returns. However, in the event of a sudden economic downturn, there is a strong case for yields to fall significantly – especially on short and medium-dated bonds – and for further price gains. This asymmetrical opportunity for gains in an otherwise difficult environment makes bonds attractive.

3. Diversification benefits from bonds possible again

With the option of capital gains in economic downturns, government bonds regain their traditional role in stabilising a diversified asset structure. This is evident in the bond-equity combination of a mixed fund that benefits from the negative correlation between equity and bond prices. It is also evident in investments in corporate bonds, which represent a combination of secure interest and risk premium. When fears suddenly arose in August 2024 that the economy could cool down, risk premiums on European corporate bonds rose slightly. At the same time, however, the yield on German government bonds fell significantly, causing the total return on the asset class to fall and prices to rise.

4. Comparably stable investment opportunities are opening up in government bonds.

A breakdown of corporate bond yields into their individual components shows that the increase in yields from 2021 to 2023 was hardly caused by rising risk premiums. Rather, the increase in the safe interest rate, i.e. the government bond component contained in these securities, provided the boost. This risk premium remains at a low level. For European corporate bonds with good credit ratings, it is around one per cent, which is about one third of the total return of 3.3 per cent and below the historical average.

Should we expect a significant widening of the yield gap between government and corporate bonds again in the coming months? We think this is unlikely. One reason for this is the good credit ratings of the issuing companies. Balance sheet analyses show solid profit growth, above-average return on sales and a debt ratio that has fallen significantly again since the coronavirus pandemic. The business performance of these companies does not therefore indicate an increased risk of insolvency, which is reflected in the ongoing rating improvements of many companies.

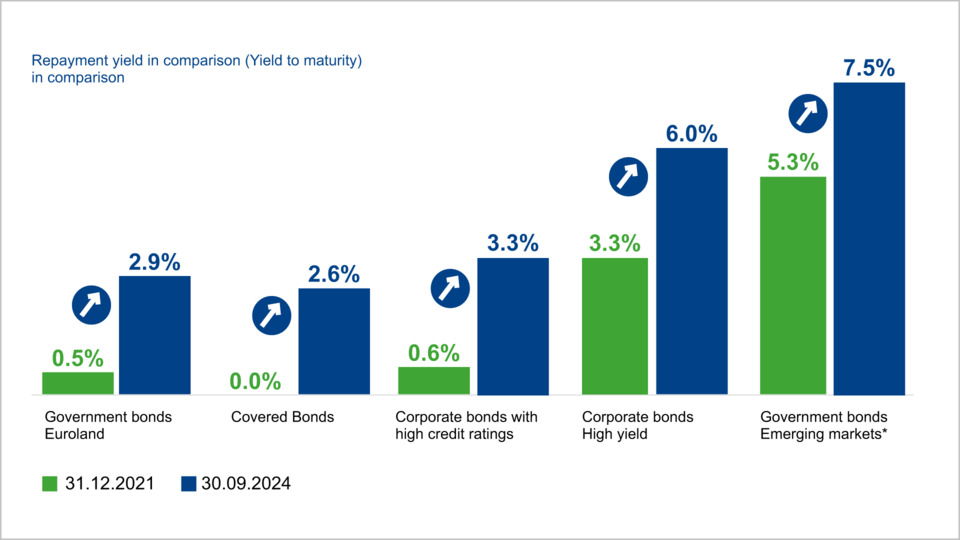

Corporate bonds are becoming increasingly interesting.

Bond market yields have improved significantly compared to the end of 2021.

Source: Union Investment, LSEG, Bloomberg, GCP, ICE BofA Merrill Lynch. As at: 30 September 2024. * Hard currency

Another reason not to expect a significant widening of the yield gap between government and corporate bonds is the rising level of government debt. In Europe, we are accustomed to an environment in which interest rate swaps and corporate bonds always yield more than German government bonds, which are considered a safe haven. But this relationship is not set in stone.

In the US, government bonds have long traded at a higher yield than interest rate swaps, in which market participants exchange fixed for variable interest rates. The fact that US Treasuries have a higher yield than these interest rate derivatives reflects the comparatively high supply of these securities. In the eurozone, too, government bonds of many countries trade at a yield premium to interest rate swaps. The exception here was German Bunds. But this is starting to change. Yields on 30-year interest rate swaps are already below those of 30-year German government bonds, and the 10-year swap spread between German government bonds and interest rate swaps has fallen to a historic low. This is due to the increased supply of government bonds on the market after the national central banks in the eurozone ended their bond-buying programmes and are no longer absorbing all new government bond issues.

The old certainty that government bonds are always less risky than corporate bonds and therefore have a lower yield is also increasingly being questioned. For example, bonds issued by the French luxury goods group LVMH have traditionally traded at a higher yield than French government bonds. Since the beginning of October 2024 this relationship has been reversed. A similar development can be seen when comparing the bonds of the Italian ENI group with Italian government bonds.

Will LVMH soon be more trustworthy than the French state?

New elections and budget problems are worsening France's creditworthiness.

There are structural breaks in the bond market. If the risk premium on corporate bonds narrows significantly, in our view this is not an indication that it will quickly return to the historical mean; instead, the narrowing could go even further this time and last longer. ‘This time is different’ can be said here. The good credit ratings of many companies and the increasing net supply of government bonds could, in individual cases, lead to a reversal of this historically stable relationship.